Predicting Loan Repayment- Analyzing LendingClub Data for Credit Risk Assessment

LendingClub is a US peer-to-peer lending company, headquartered in San Francisco, California[3]. It was the first peer-to-peer lender to register its offerings as securities with the Securities and Exchange Commission (SEC), and to offer loan trading on a secondary market. LendingClub is the world’s largest peer-to-peer lending platform.

I used a subset of the LendingClub DataSet obtained from Kaggle: https://www.kaggle.com/wordsforthewise/lending-club

Given historical data on loans given out with information on whether or not the borrower defaulted (charge-off), I built a model to predict whether or not a borrower would pay back their loan? This way in the future when we get a new potential customer we can assess whether or not they are likely to pay back the loan.

The “loan_status” column contains the label.

Data Overview

Here is the information on this particular data set:

| LoanStatNew | Description | |

|---|---|---|

| 0 | loan_amnt | The listed amount of the loan applied for by the borrower. If at some point in time, the credit department reduces the loan amount, then it will be reflected in this value. |

| 1 | term | The number of payments on the loan. Values are in months and can be either 36 or 60. |

| 2 | int_rate | Interest Rate on the loan |

| 3 | installment | The monthly payment owed by the borrower if the loan originates. |

| 4 | grade | LC assigned loan grade |

| 5 | sub_grade | LC assigned loan subgrade |

| 6 | emp_title | The job title supplied by the Borrower when applying for the loan.* |

| 7 | emp_length | Employment length in years. Possible values are between 0 and 10 where 0 means less than one year and 10 means ten or more years. |

| 8 | home_ownership | The home ownership status provided by the borrower during registration or obtained from the credit report. Our values are: RENT, OWN, MORTGAGE, OTHER |

| 9 | annual_inc | The self-reported annual income provided by the borrower during registration. |

| 10 | verification_status | Indicates if income was verified by LC, not verified, or if the income source was verified |

| 11 | issue_d | The month which the loan was funded |

| 12 | loan_status | Current status of the loan |

| 13 | purpose | A category provided by the borrower for the loan request. |

| 14 | title | The loan title provided by the borrower |

| 15 | zip_code | The first 3 numbers of the zip code provided by the borrower in the loan application. |

| 16 | addr_state | The state provided by the borrower in the loan application |

| 17 | dti | A ratio calculated using the borrower’s total monthly debt payments on the total debt obligations, excluding mortgage and the requested LC loan, divided by the borrower’s self-reported monthly income. |

| 18 | earliest_cr_line | The month the borrower's earliest reported credit line was opened |

| 19 | open_acc | The number of open credit lines in the borrower's credit file. |

| 20 | pub_rec | Number of derogatory public records |

| 21 | revol_bal | Total credit revolving balance |

| 22 | revol_util | Revolving line utilization rate, or the amount of credit the borrower is using relative to all available revolving credit. |

| 23 | total_acc | The total number of credit lines currently in the borrower's credit file |

| 24 | initial_list_status | The initial listing status of the loan. Possible values are – W, F |

| 25 | application_type | Indicates whether the loan is an individual application or a joint application with two co-borrowers |

| 26 | mort_acc | Number of mortgage accounts. |

| 27 | pub_rec_bankruptcies | Number of public record bankruptcies |

Import Required Packages and Data

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import seaborn as sns

df = pd.read_csv('../DATA/lending_club_loan_two.csv')

df.info()

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 396030 entries, 0 to 396029

Data columns (total 27 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 loan_amnt 396030 non-null float64

1 term 396030 non-null object

2 int_rate 396030 non-null float64

3 installment 396030 non-null float64

4 grade 396030 non-null object

5 sub_grade 396030 non-null object

6 emp_title 373103 non-null object

7 emp_length 377729 non-null object

8 home_ownership 396030 non-null object

9 annual_inc 396030 non-null float64

10 verification_status 396030 non-null object

11 issue_d 396030 non-null object

12 loan_status 396030 non-null object

13 purpose 396030 non-null object

14 title 394275 non-null object

15 dti 396030 non-null float64

16 earliest_cr_line 396030 non-null object

17 open_acc 396030 non-null float64

18 pub_rec 396030 non-null float64

19 revol_bal 396030 non-null float64

20 revol_util 395754 non-null float64

21 total_acc 396030 non-null float64

22 initial_list_status 396030 non-null object

23 application_type 396030 non-null object

24 mort_acc 358235 non-null float64

25 pub_rec_bankruptcies 395495 non-null float64

26 address 396030 non-null object

dtypes: float64(12), object(15)

memory usage: 81.6+ MB

df.head()

| loan_amnt | term | int_rate | installment | grade | sub_grade | emp_title | emp_length | home_ownership | annual_inc | ... | open_acc | pub_rec | revol_bal | revol_util | total_acc | initial_list_status | application_type | mort_acc | pub_rec_bankruptcies | address | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 10000.0 | 36 months | 11.44 | 329.48 | B | B4 | Marketing | 10+ years | RENT | 117000.0 | ... | 16.0 | 0.0 | 36369.0 | 41.8 | 25.0 | w | INDIVIDUAL | 0.0 | 0.0 | 0174 Michelle Gateway\nMendozaberg, OK 22690 |

| 1 | 8000.0 | 36 months | 11.99 | 265.68 | B | B5 | Credit analyst | 4 years | MORTGAGE | 65000.0 | ... | 17.0 | 0.0 | 20131.0 | 53.3 | 27.0 | f | INDIVIDUAL | 3.0 | 0.0 | 1076 Carney Fort Apt. 347\nLoganmouth, SD 05113 |

| 2 | 15600.0 | 36 months | 10.49 | 506.97 | B | B3 | Statistician | < 1 year | RENT | 43057.0 | ... | 13.0 | 0.0 | 11987.0 | 92.2 | 26.0 | f | INDIVIDUAL | 0.0 | 0.0 | 87025 Mark Dale Apt. 269\nNew Sabrina, WV 05113 |

| 3 | 7200.0 | 36 months | 6.49 | 220.65 | A | A2 | Client Advocate | 6 years | RENT | 54000.0 | ... | 6.0 | 0.0 | 5472.0 | 21.5 | 13.0 | f | INDIVIDUAL | 0.0 | 0.0 | 823 Reid Ford\nDelacruzside, MA 00813 |

| 4 | 24375.0 | 60 months | 17.27 | 609.33 | C | C5 | Destiny Management Inc. | 9 years | MORTGAGE | 55000.0 | ... | 13.0 | 0.0 | 24584.0 | 69.8 | 43.0 | f | INDIVIDUAL | 1.0 | 0.0 | 679 Luna Roads\nGreggshire, VA 11650 |

5 rows × 27 columns

Part1: Exploratory Data Analysis

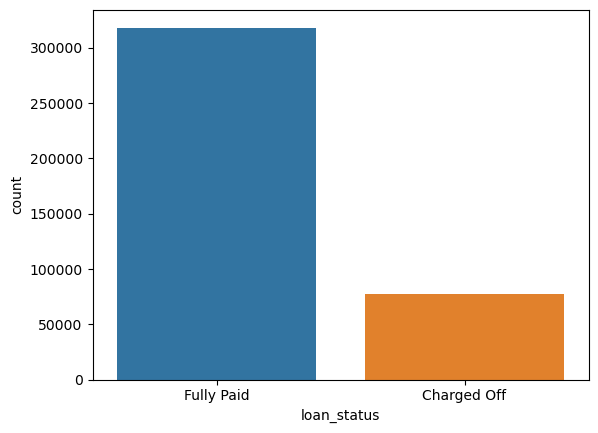

Since I wanted to predict loan_status, I created a countplot as shown below to see how balanced the labels were:

sns.countplot(x='loan_status', data=df)

<Axes: xlabel='loan_status', ylabel='count'>

I had an imbalanced dataset. I expected to do very well in terms of accuracy but I had to use recall and precision to evaluate my data.

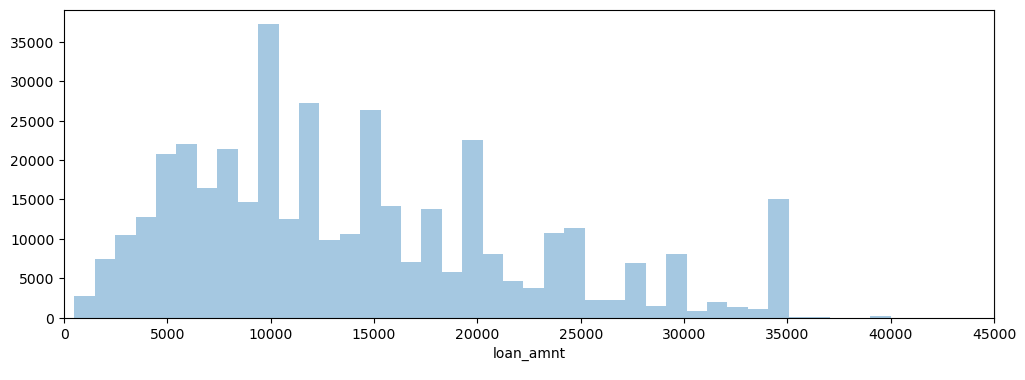

I created a histogram of the loan_amnt column.

plt.figure(figsize=(9,4))

sns.histplot(data=df,x='loan_amnt', bins=40)

<Axes: xlabel='loan_amnt', ylabel='Count'>

It showed that the vast majority of loans were between 5000 and 25000$.

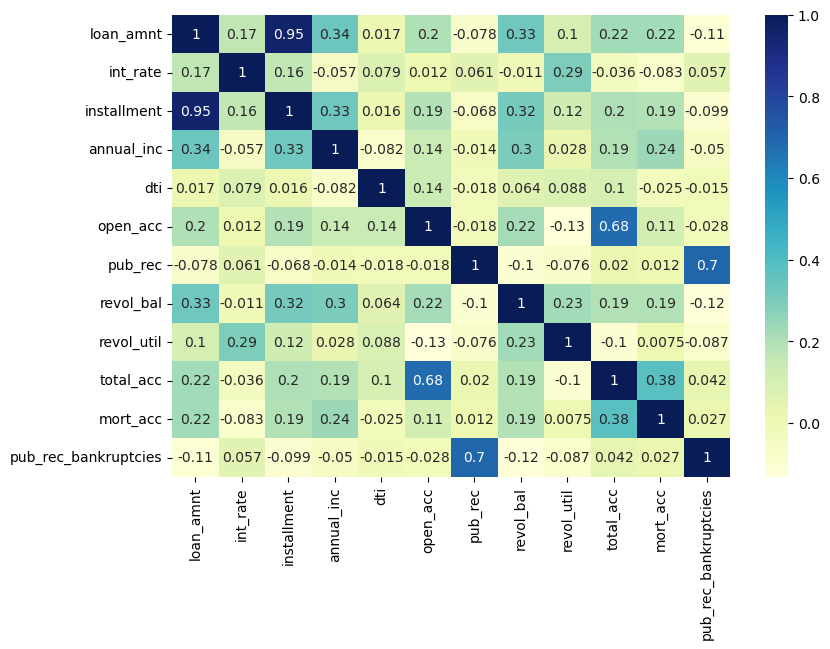

I then explored correlation between the continuous feature variables and visualize it using heatmap.

df.corr()

| loan_amnt | int_rate | installment | annual_inc | dti | open_acc | pub_rec | revol_bal | revol_util | total_acc | mort_acc | pub_rec_bankruptcies | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| loan_amnt | 1.000000 | 0.168921 | 0.953929 | 0.336887 | 0.016636 | 0.198556 | -0.077779 | 0.328320 | 0.099911 | 0.223886 | 0.222315 | -0.106539 |

| int_rate | 0.168921 | 1.000000 | 0.162758 | -0.056771 | 0.079038 | 0.011649 | 0.060986 | -0.011280 | 0.293659 | -0.036404 | -0.082583 | 0.057450 |

| installment | 0.953929 | 0.162758 | 1.000000 | 0.330381 | 0.015786 | 0.188973 | -0.067892 | 0.316455 | 0.123915 | 0.202430 | 0.193694 | -0.098628 |

| annual_inc | 0.336887 | -0.056771 | 0.330381 | 1.000000 | -0.081685 | 0.136150 | -0.013720 | 0.299773 | 0.027871 | 0.193023 | 0.236320 | -0.050162 |

| dti | 0.016636 | 0.079038 | 0.015786 | -0.081685 | 1.000000 | 0.136181 | -0.017639 | 0.063571 | 0.088375 | 0.102128 | -0.025439 | -0.014558 |

| open_acc | 0.198556 | 0.011649 | 0.188973 | 0.136150 | 0.136181 | 1.000000 | -0.018392 | 0.221192 | -0.131420 | 0.680728 | 0.109205 | -0.027732 |

| pub_rec | -0.077779 | 0.060986 | -0.067892 | -0.013720 | -0.017639 | -0.018392 | 1.000000 | -0.101664 | -0.075910 | 0.019723 | 0.011552 | 0.699408 |

| revol_bal | 0.328320 | -0.011280 | 0.316455 | 0.299773 | 0.063571 | 0.221192 | -0.101664 | 1.000000 | 0.226346 | 0.191616 | 0.194925 | -0.124532 |

| revol_util | 0.099911 | 0.293659 | 0.123915 | 0.027871 | 0.088375 | -0.131420 | -0.075910 | 0.226346 | 1.000000 | -0.104273 | 0.007514 | -0.086751 |

| total_acc | 0.223886 | -0.036404 | 0.202430 | 0.193023 | 0.102128 | 0.680728 | 0.019723 | 0.191616 | -0.104273 | 1.000000 | 0.381072 | 0.042035 |

| mort_acc | 0.222315 | -0.082583 | 0.193694 | 0.236320 | -0.025439 | 0.109205 | 0.011552 | 0.194925 | 0.007514 | 0.381072 | 1.000000 | 0.027239 |

| pub_rec_bankruptcies | -0.106539 | 0.057450 | -0.098628 | -0.050162 | -0.014558 | -0.027732 | 0.699408 | -0.124532 | -0.086751 | 0.042035 | 0.027239 | 1.000000 |

plt.figure(figsize=(9,6))

sns.heatmap(df.corr(), annot=True, cmap='YlGnBu')

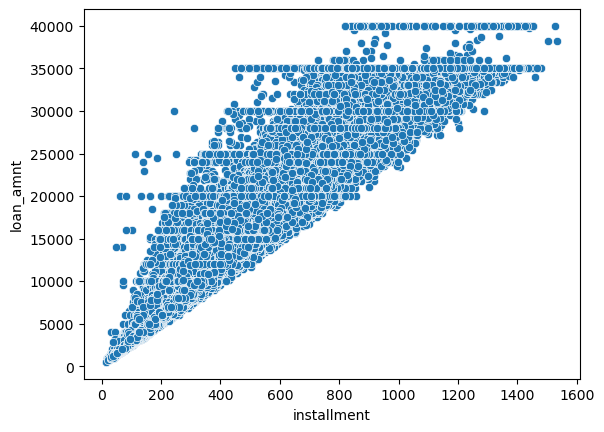

I noticed an almost perfect correlation between the loan amount and “installment” features and tried to explore these features further. For that, I first found their description and then drew a scatterplot between them.

data_info = pd.read_csv('../DATA/lending_club_info.csv',index_col='LoanStatNew')

def feature_info(col_name):

print(data_info.loc[col_name]['Description'])

feature_info('installment')

The monthly payment owed by the borrower if the loan originates.

feature_info('loan_amnt')

The listed amount of the loan applied for by the borrower. If at some point in time, the credit department reduces the loan amount, then it will be reflected in this value.

sns.scatterplot(y='loan_amnt', x='installment', data=df)

A perfect correlation was noticed between these two features.

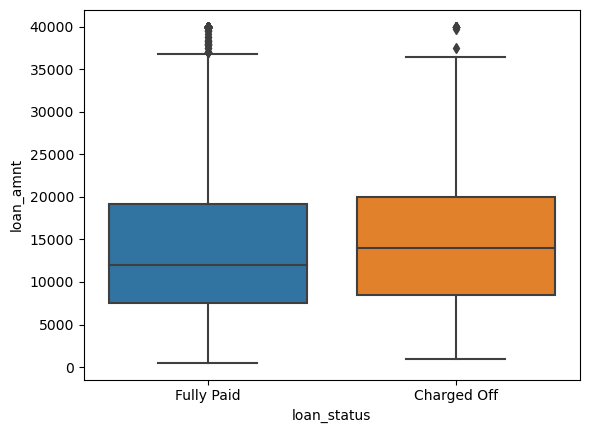

I tried to see if there was any relationship between the loan status and the amount of the loan. For that, I created a boxplot.

sns.boxplot(data=df, x='loan_status', y='loan_amnt')

They looked pretty similar.

Then, I calculated the summary statistics for the loan amount, grouped by the loan_status.

df.groupby('loan_status')['loan_amnt'].describe()

| count | mean | std | min | 25% | 50% | 75% | max | |

|---|---|---|---|---|---|---|---|---|

| loan_status | ||||||||

| Charged Off | 77673.0 | 15126.300967 | 8505.090557 | 1000.0 | 8525.0 | 14000.0 | 20000.0 | 40000.0 |

| Fully Paid | 318357.0 | 13866.878771 | 8302.319699 | 500.0 | 7500.0 | 12000.0 | 19225.0 | 40000.0 |

The average loan amount of the charged-off group was a little higher than fully paid ones which made sense as higher loan amounts were more difficult to pay off.

I explored the Grade and SubGrade columns that LendingClub attributed to the loans and checked the unique possible grades and subgrades.

grade_order = sorted(df['grade'].unique())

Subgrade_order = sorted(df['sub_grade'].unique())

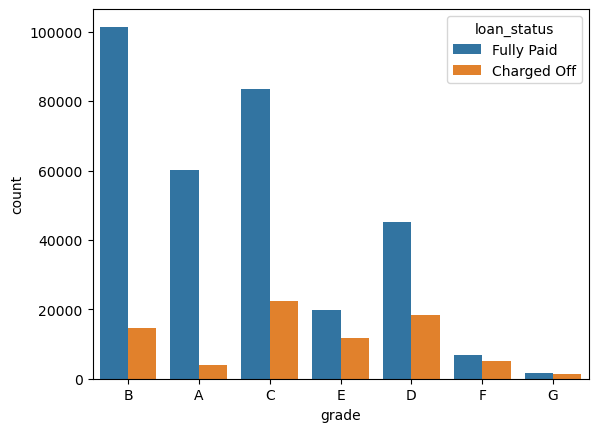

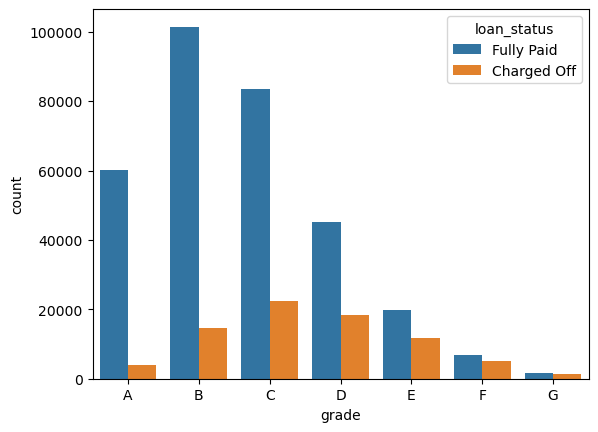

I created a countplot per grade to see the loan status . I set the hue to the loan_status label.

sns.countplot(x='grade', hue='loan_status', data=df)

<Axes: xlabel='grade', ylabel='count'>

I ordered the bars from grade A to E

sns.countplot(x='grade', hue='loan_status', data=df, order=grade_order)

<Axes: xlabel='grade', ylabel='count'>

Moving from grade A to G, the ratio of fully paid loans to charged off loans decreased meaning that we faced riskier groups.

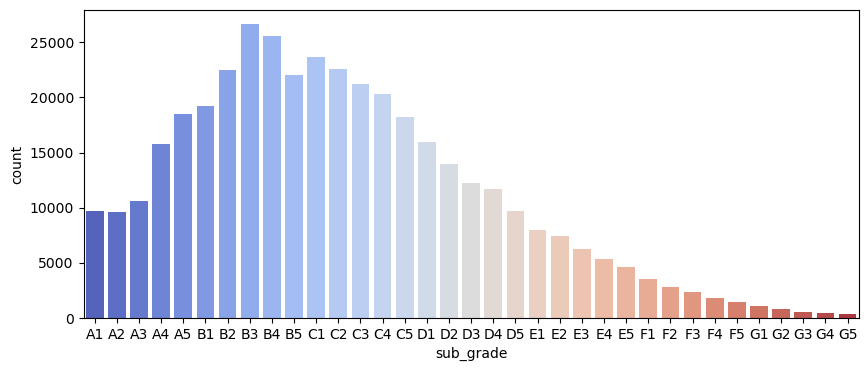

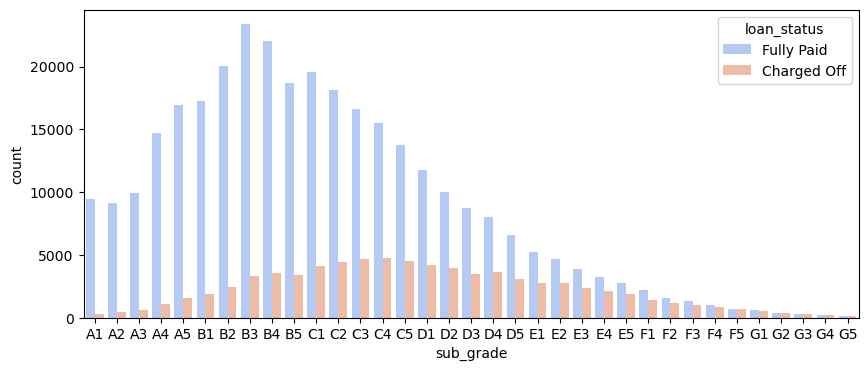

I drew a count plot per subgrade.

plt.figure(figsize=(10,4))

sns.countplot(x='sub_grade', data=df, order=Subgrade_order, palette='coolwarm')

<Axes: xlabel='sub_grade', ylabel='count'>

A decrease in the number of loans was seen when moving from sub_grades A to G which makde sense as we moved towards riskier groups.

Then, I checked all loans made per subgrade separated based on the loan_status.

plt.figure(figsize=(10,4))

sns.countplot(x='sub_grade', data=df, order=Subgrade_order, hue='loan_status', palette='coolwarm')

<Axes: xlabel='sub_grade', ylabel='count'>

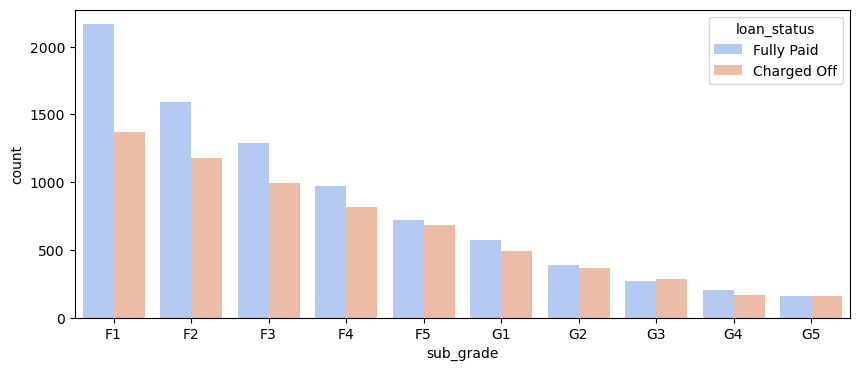

It looked like F and G subgrades didn’t get paid back that often. I isolated those and recreated the countplot just for those subgrades.

F_and_G = df[(df['grade']=='F')|(df['grade']=='G')]

F_and_G_sub_grade_order = sorted((F_and_G)['sub_grade'].unique())

plt.figure(figsize=(10,4))

sns.countplot(x='sub_grade', data=df, order=F_and_G_sub_grade_order, hue='loan_status', palette='coolwarm')

<Axes: xlabel='sub_grade', ylabel='count'>

As shown in the above figure, the number of fully paid loans was almost equal to the number of charged-off ones for grades F and G.

Id create a new column called ‘loan_repaid’ which contained a 1 if the loan status was “Fully Paid” and a 0 if it was “Charged Off”.**

def status(x):

if x=='Fully Paid':

return 1

else:

return 0

df['loan_repaid'] = df['loan_status'].apply(status)

| loan_repaid | loan_status | |

|---|---|---|

| 0 | 1 | Fully Paid |

| 1 | 1 | Fully Paid |

| 2 | 1 | Fully Paid |

| 3 | 1 | Fully Paid |

| 4 | 0 | Charged Off |

| ... | ... | ... |

| 396025 | 1 | Fully Paid |

| 396026 | 1 | Fully Paid |

| 396027 | 1 | Fully Paid |

| 396028 | 1 | Fully Paid |

| 396029 | 1 | Fully Paid |

396030 rows × 2 columns

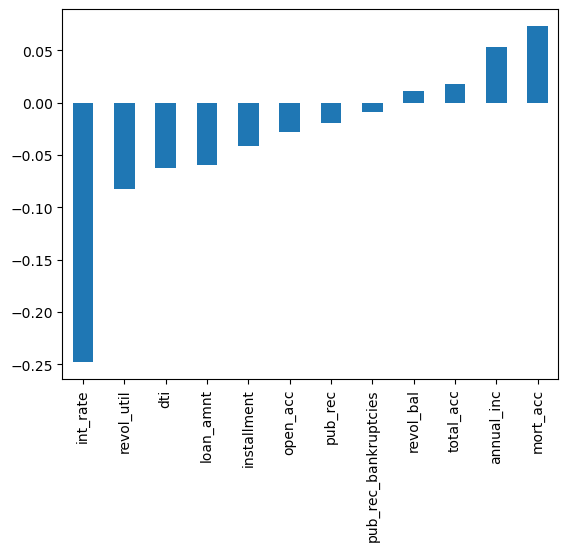

df.corr()['loan_repaid'].sort_values().drop('loan_repaid').plot(kind='bar')

The interest rate had the highest negative correlation with loan_repaid which totally made sense as higher interest rate made it more difficult to repay the loan.

Part 2: Data PreProcessing

df.head()

| loan_amnt | term | int_rate | installment | grade | sub_grade | emp_title | emp_length | home_ownership | annual_inc | ... | pub_rec | revol_bal | revol_util | total_acc | initial_list_status | application_type | mort_acc | pub_rec_bankruptcies | address | loan_repaid | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 10000.0 | 36 months | 11.44 | 329.48 | B | B4 | Marketing | 10+ years | RENT | 117000.0 | ... | 0.0 | 36369.0 | 41.8 | 25.0 | w | INDIVIDUAL | 0.0 | 0.0 | 0174 Michelle Gateway\nMendozaberg, OK 22690 | 1 |

| 1 | 8000.0 | 36 months | 11.99 | 265.68 | B | B5 | Credit analyst | 4 years | MORTGAGE | 65000.0 | ... | 0.0 | 20131.0 | 53.3 | 27.0 | f | INDIVIDUAL | 3.0 | 0.0 | 1076 Carney Fort Apt. 347\nLoganmouth, SD 05113 | 1 |

| 2 | 15600.0 | 36 months | 10.49 | 506.97 | B | B3 | Statistician | < 1 year | RENT | 43057.0 | ... | 0.0 | 11987.0 | 92.2 | 26.0 | f | INDIVIDUAL | 0.0 | 0.0 | 87025 Mark Dale Apt. 269\nNew Sabrina, WV 05113 | 1 |

| 3 | 7200.0 | 36 months | 6.49 | 220.65 | A | A2 | Client Advocate | 6 years | RENT | 54000.0 | ... | 0.0 | 5472.0 | 21.5 | 13.0 | f | INDIVIDUAL | 0.0 | 0.0 | 823 Reid Ford\nDelacruzside, MA 00813 | 1 |

| 4 | 24375.0 | 60 months | 17.27 | 609.33 | C | C5 | Destiny Management Inc. | 9 years | MORTGAGE | 55000.0 | ... | 0.0 | 24584.0 | 69.8 | 43.0 | f | INDIVIDUAL | 1.0 | 0.0 | 679 Luna Roads\nGreggshire, VA 11650 | 0 |

5 rows × 28 columns

Missing Data

I used a variety of factors to decide whether or not they would be useful, and to see if I should keep, discard, or fill in the missing data.

Length of the dataframe:

df_length = len(df)

Total count of missing values per column:

df.isna().sum()

loan_amnt 0

term 0

int_rate 0

installment 0

grade 0

sub_grade 0

emp_title 22927

emp_length 18301

home_ownership 0

annual_inc 0

verification_status 0

issue_d 0

loan_status 0

purpose 0

title 1755

dti 0

earliest_cr_line 0

open_acc 0

pub_rec 0

revol_bal 0

revol_util 276

total_acc 0

initial_list_status 0

application_type 0

mort_acc 37795

pub_rec_bankruptcies 535

address 0

loan_repaid 0

dtype: int64

Total percentage of missing values per column:

df.isna().sum()/(df_length)*100

loan_amnt 0.000000

term 0.000000

int_rate 0.000000

installment 0.000000

grade 0.000000

sub_grade 0.000000

emp_title 5.789208

emp_length 4.621115

home_ownership 0.000000

annual_inc 0.000000

verification_status 0.000000

issue_d 0.000000

loan_status 0.000000

purpose 0.000000

title 0.443148

dti 0.000000

earliest_cr_line 0.000000

open_acc 0.000000

pub_rec 0.000000

revol_bal 0.000000

revol_util 0.069692

total_acc 0.000000

initial_list_status 0.000000

application_type 0.000000

mort_acc 9.543469

pub_rec_bankruptcies 0.135091

address 0.000000

loan_repaid 0.000000

dtype: float64

I examined emp_title and emp_length to see whether it would be okay to drop them.

feature_info('emp_title')

The job title supplied by the Borrower when applying for the loan.

feature_info('emp_length')

Employment length in years. Possible values were between 0 and 10 where 0 meant less than one year and 10 meant ten or more years.

Number of unique employment job titles:

df['emp_title'].nunique()

173105

df['emp_title'].value_counts()

Teacher 4389

Manager 4250

Registered Nurse 1856

RN 1846

Supervisor 1830

...

Postman 1

McCarthy & Holthus, LLC 1

jp flooring 1

Histology Technologist 1

Gracon Services, Inc 1

Name: emp_title, Length: 173105, dtype: int64

Realistically there were too many unique job titles to try to convert to numeric feature. Therefore, I removed that emp_title column.

df = df.drop('emp_title', axis=1)

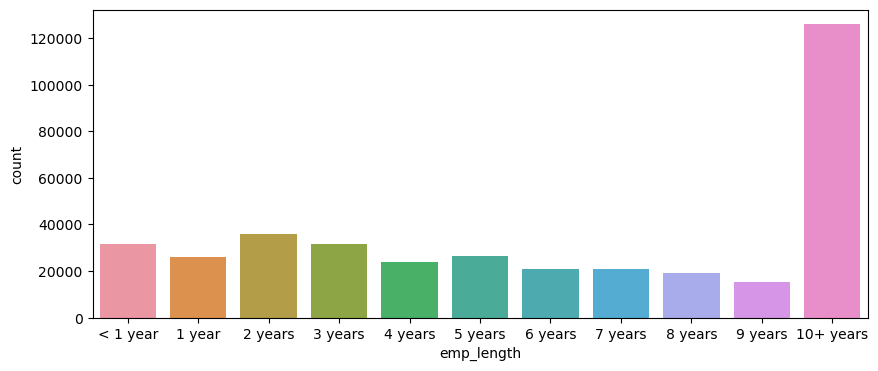

I created a count plot of the emp_length feature column, sorted by the order of the values.

df['emp_length'].dropna().unique()

['1 year',

'10+ years',

'2 years',

'3 years',

'4 years',

'5 years',

'6 years',

'7 years',

'8 years',

'9 years',

'< 1 year']

emp_length_order = sorted(df['emp_length'].dropna().unique())

emp_length_order = [ ‘< 1 year’, ‘1 year’, ‘2 years’, ‘3 years’, ‘4 years’, ‘5 years’, ‘6 years’, ‘7 years’, ‘8 years’, ‘9 years’, ‘10+ years’]

```python

plt.figure(figsize=(10,4))

sns.countplot(data=df, x='emp_length', order=emp_length_order)

It seemed that the majority of people who took loan had been working for more than 10 years which made sense as I had to have a kind of job security to be able to repay the loan.

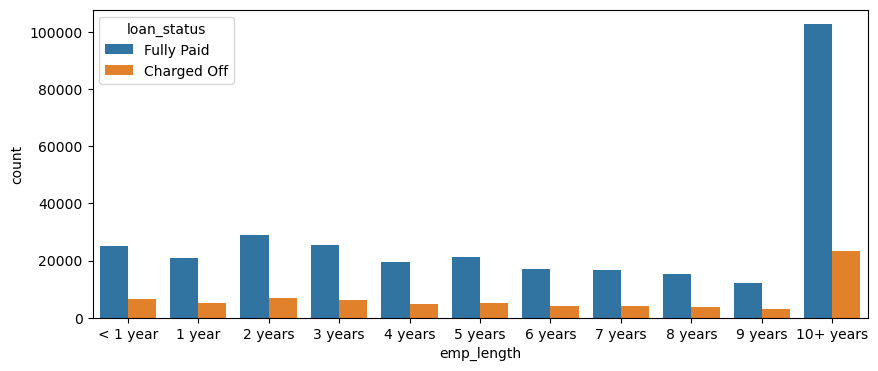

I plotted out the countplot with a hue separating Fully Paid vs Charged Off

plt.figure(figsize=(10,4))

sns.countplot(data=df, x='emp_length', order=emp_length_order, hue= 'loan_status')

For people with more than 10+ years of employment length, the number of fully paid loans was much higher than charged-off ones.

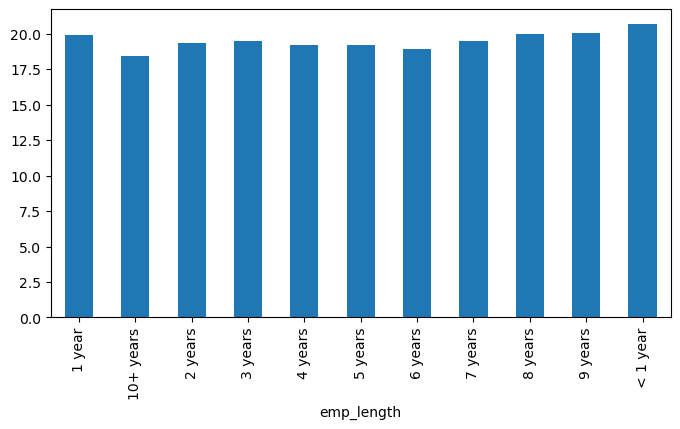

I found the percentage of charge-offs per category to see what percent of people per employment category didn’t pay back their loan. It might help me to understand if there was a strong relationship between employment length and being charged off.

fully_paid_number = df[df['loan_status']=='Fully Paid'].groupby('emp_length').count()['loan_status']

charged_off_number = df[df['loan_status']=='Charged Off'].groupby('emp_length').count()['loan_status']

total_loan_number = fully_paid_number + charged_off_number

charged_off_percentage = charged_off_number/total_loan_number*100

plt.figure(figsize=(8,4))

charged_off_percentage.plot(kind='bar')

Charge off rates were similar across all employment lengths.

Then, I dropped the emp_length column.

df = df.drop('emp_length', axis=1)

I revisited the DataFrame to see what feature columns still had missing data.

df.isna().sum()

loan_amnt 0

term 0

int_rate 0

installment 0

grade 0

sub_grade 0

home_ownership 0

annual_inc 0

verification_status 0

issue_d 0

loan_status 0

purpose 0

title 1755

dti 0

earliest_cr_line 0

open_acc 0

pub_rec 0

revol_bal 0

revol_util 276

total_acc 0

initial_list_status 0

application_type 0

mort_acc 37795

pub_rec_bankruptcies 535

address 0

loan_repaid 0

dtype: int64

Then I reviewed the title column vs the purpose column to see if there was any repeated information.

df['purpose'].head(10)

0 vacation

1 debt_consolidation

2 credit_card

3 credit_card

4 credit_card

5 debt_consolidation

6 home_improvement

7 credit_card

8 debt_consolidation

9 debt_consolidation

Name: purpose, dtype: object

df['title'].head(10)

0 Vacation

1 Debt consolidation

2 Credit card refinancing

3 Credit card refinancing

4 Credit Card Refinance

5 Debt consolidation

6 Home improvement

7 No More Credit Cards

8 Debt consolidation

9 Debt Consolidation

Name: title, dtype: object

It seemed that the title column was simply a string subcategory/description of the purpose column. Therefore, I dropped the title column.

df = df.drop('title', axis=1)

I tried to find out what the mort_acc feature represented.

feature_info('mort_acc')

Number of mortgage accounts.

I created a value_counts of the mort_acc column.

df['mort_acc'].value_counts()

0.0 139777

1.0 60416

2.0 49948

3.0 38049

4.0 27887

5.0 18194

6.0 11069

7.0 6052

8.0 3121

9.0 1656

10.0 865

11.0 479

12.0 264

13.0 146

14.0 107

15.0 61

16.0 37

17.0 22

18.0 18

19.0 15

20.0 13

24.0 10

22.0 7

21.0 4

25.0 4

27.0 3

32.0 2

31.0 2

23.0 2

26.0 2

28.0 1

30.0 1

34.0 1

Name: mort_acc, dtype: int64

Then, I reviewed the other columns to see which most highly correlates to mort_acc.

df.corr()['mort_acc'].sort_values()

int_rate -0.082583

dti -0.025439

revol_util 0.007514

pub_rec 0.011552

pub_rec_bankruptcies 0.027239

loan_repaid 0.073111

open_acc 0.109205

installment 0.193694

revol_bal 0.194925

loan_amnt 0.222315

annual_inc 0.236320

total_acc 0.381072

mort_acc 1.000000

Name: mort_acc, dtype: float64

I Looked like the total_acc feature correlated with the mort_acc , this made sense!

feature_info('total_acc')

The total number of credit lines currently in the borrower's credit file

I tried the fillna() approach to replace missing data. I grouped the dataframe by the total_acc and calculated the mean value for the mort_acc per total_acc entry.

df_acc = df[['total_acc','mort_acc']].sort_values(by='total_acc')

df_acc

mort_acc_mean = df.groupby('total_acc')['mort_acc'].mean()

I filled in the missing mort_acc values based on their total_acc value. If the mort_acc was missing, then I filled in that missing value with the mean value corresponding to its total_acc value.

mort_acc_mean = pd.DataFrame(mort_acc_mean)

mort_acc_mean.columns = ['mort_acc_mean']

df_acc = df_acc.merge(mort_acc_mean, on='total_acc', how='inner')

df['mort_acc'].fillna(value=df_acc['mort_acc_mean'], inplace=True)

df.isna().sum()

revol_util and the pub_rec_bankruptcies had missing data points, but they accounted for less than 0.5% of the total data. Therefore, I removed the rows that were missing those values in those columns.

df = df.dropna()

df.isna().sum()

loan_amnt 0

term 0

int_rate 0

installment 0

grade 0

sub_grade 0

home_ownership 0

annual_inc 0

verification_status 0

issue_d 0

loan_status 0

purpose 0

dti 0

earliest_cr_line 0

open_acc 0

pub_rec 0

revol_bal 0

revol_util 276

total_acc 0

initial_list_status 0

application_type 0

mort_acc 37795

pub_rec_bankruptcies 535

address 0

loan_repaid 0

dtype: int64

Categorical Variables

Here, I Listed all the columns that were non-numeric.

df.select_dtypes(['object']).columns

Index(['term', 'grade', 'sub_grade', 'home_ownership', 'verification_status',

'issue_d', 'loan_status', 'purpose', 'earliest_cr_line',

'initial_list_status', 'application_type', 'address'],

dtype='object')

term feature

df['term'].value_counts()

36 months 302005

60 months 94025

Name: term, dtype: int64

term feature had just 2 values of 36 and 60 months. I removed the month and simply converted the categorical data to numeric one.

def conversion(x):

return int(x[1:3])

df['term'] = df['term'].apply(conversion)

# Alternative: df['term'] = df['term'].apply(lambda term: int(term[:3]))

df['term'].value_counts()

36 302005

60 94025

Name: term, dtype: int64

grade feature: I already knew grade was part of sub_grade, so I dropped the grade feature.

df = df.drop('grade', axis=1)

sub_grade feature: I kept it to convert it to a numeric feature later on.

home_ownership feature:

df['home_ownership'].value_counts()

MORTGAGE 198348

RENT 159790

OWN 37746

OTHER 112

NONE 31

ANY 3

Name: home_ownership, dtype: int64

df['verification_status'].value_counts()

Verified 139563

Source Verified 131385

Not Verified 125082

Name: verification_status, dtype: int64

issue_d feature

df['issue_d'].value_counts()

Oct-2014 14846

Jul-2014 12609

Jan-2015 11705

Dec-2013 10618

Nov-2013 10496

...

Jul-2007 26

Sep-2008 25

Nov-2007 22

Sep-2007 15

Jun-2007 1

Name: issue_d, Length: 115, dtype: int64

This was data leakage as I wouldn’t know beforehand whether or not a loan would be issued when using my model, so in theory, I wouldn’t have an issue_date. I dropped this feature.

df = df = df.drop('issue_d', axis=1)

loan_status feature: As loan_status column was a duplicate of the loan_repaid column, I dropped the load_status column and used the loan_repaid column since its already in 0s and 1s.

df = df.drop('loan_status', axis=1)

purpose feature

df['purpose'].value_counts()

debt_consolidation 234507

credit_card 83019

home_improvement 24030

other 21185

major_purchase 8790

small_business 5701

car 4697

medical 4196

moving 2854

vacation 2452

house 2201

wedding 1812

renewable_energy 329

educational 257

Name: purpose, dtype: int64

earliest_cr_line feature

df['earliest_cr_line'].value_counts()

Oct-2000 3017

Aug-2000 2935

Oct-2001 2896

Aug-2001 2884

Nov-2000 2736

...

Jul-1958 1

Nov-1957 1

Jan-1953 1

Jul-1955 1

Aug-1959 1

Name: earliest_cr_line, Length: 684, dtype: int64

This appeareds to be a historical time stamp feature. I extracted the year from this feature and converted it to a numeric feature.

def year(x):

return int(x[4:])

df['earliest_cr_line'].apply(year)

0 1990

1 2004

2 2007

3 2006

4 1999

...

396025 2004

396026 2006

396027 1997

396028 1990

396029 1998

Name: earliest_cr_line, Length: 396030, dtype: int64

I set this new data to a feature column called ‘earliest_cr_year’.Then dropped the earliest_cr_line feature.

df['earliest_cr_year']= df['earliest_cr_line'].apply(year)

df = df.drop('earliest_cr_line', axis=1)

initial_list_status feature

df['initial_list_status'].value_counts()

f 238066

w 157964

Name: initial_list_status, dtype: int64

application_type feature

df['application_type'].value_counts()

INDIVIDUAL 395319

JOINT 425

DIRECT_PAY 286

Name: application_type, dtype: int64

address feature

df['address'].value_counts()

USCGC Smith\nFPO AE 70466 8

USS Johnson\nFPO AE 48052 8

USNS Johnson\nFPO AE 05113 8

USS Smith\nFPO AP 70466 8

USNS Johnson\nFPO AP 48052 7

..

455 Tricia Cove\nAustinbury, FL 00813 1

7776 Flores Fall\nFernandezshire, UT 05113 1

6577 Mia Harbors Apt. 171\nRobertshire, OK 22690 1

8141 Cox Greens Suite 186\nMadisonstad, VT 05113 1

787 Michelle Causeway\nBriannaton, AR 48052 1

Name: address, Length: 393700, dtype: int64

I extracted the zip_code from address.

def zip_code(x):

return x[-5:]

df ['zip_code'] = df['address'].apply(zip_code)

I dropped address column.

df = df.drop('address', axis=1)

Applying OneHotEncoder to convert all categorical features except loan_status to numeric ones.

from sklearn.preprocessing import OneHotEncoder

# Create a list of categorical variables

categorical_vars = ['sub_grade', 'home_ownership', 'verification_status',

'purpose', 'initial_list_status', 'application_type', 'zip_code']

# Create and apply OneHotEncoder while removing the dummy variable

one_hot_encoder = OneHotEncoder(sparse = False, drop = 'first')

# Apply fit_transform on data

df_encoded = one_hot_encoder.fit_transform(df[categorical_vars])

# Get feature names to see what each column in the 'encoder_vars_array' presents

encoder_feature_names = one_hot_encoder.get_feature_names_out(categorical_vars)

# Convert our result from an array to a DataFrame

df_encoded = pd.DataFrame(df_encoded, columns = encoder_feature_names)

# Concatenate (Link together in a series or chain) new DataFrame to our original DataFrame

df = pd.concat([df.reset_index(drop = True),df_encoded.reset_index(drop = True)], axis = 1)

# Drop the original categorical variable columns

df.drop(categorical_vars, axis = 1, inplace = True)

Training Test Split

from sklearn.model_selection import train_test_split

Creating input and output variables

X = df.drop('loan_repaid', axis=1)

y = df['loan_repaid']

Due to low RAM, I grabbed a sample for data training to save time on training.

df = df.sample(frac=0.1,random_state=101)

print(len(df))

39603

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.20, random_state=101)

Normalizing the Data

from sklearn.preprocessing import MinMaxScaler

scaler = MinMaxScaler()

X_train = pd.DataFrame(scaler.fit_transform(X_train))

X_test = pd.DataFrame(scaler.transform(X_test))

Creating the Model

import tensorflow as tf

from tensorflow.keras.models import Sequential

from tensorflow.keras.layers import Dense,Dropout

X_train.shape

(316824, 80)

model = Sequential()

# input layer

model.add(Dense(80, activation='relu'))

model.add(Dropout(0.2))

# hidden layer

model.add(Dense(40, activation='relu'))

model.add(Dropout(0.2))

# hidden layer

model.add(Dense(20, activation='relu'))

model.add(Dropout(0.2))

# output layer

model.add(Dense(units=1,activation='sigmoid')) # output is either 0 or 1

# Compile model

model.compile(loss='binary_crossentropy', optimizer='adam')

fitting the model to the training data

model.fit(x=X_train,

y=y_train,

epochs=50,

batch_size=256,

validation_data=(X_test, y_test))

Epoch 1/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 6ms/step - loss: 0.5360 - val_loss: 0.4944

Epoch 2/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 5ms/step - loss: 0.4998 - val_loss: 0.4945

Epoch 3/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 6ms/step - loss: 0.4974 - val_loss: 0.4944

Epoch 4/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 6ms/step - loss: 0.4957 - val_loss: 0.4944

Epoch 5/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 6ms/step - loss: 0.4973 - val_loss: 0.4943

Epoch 6/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 6ms/step - loss: 0.4949 - val_loss: 0.4943

Epoch 7/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 6ms/step - loss: 0.4948 - val_loss: 0.4943

Epoch 8/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 5ms/step - loss: 0.4953 - val_loss: 0.4943

Epoch 9/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 4ms/step - loss: 0.4959 - val_loss: 0.4943

Epoch 10/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 5ms/step - loss: 0.4969 - val_loss: 0.4943

Epoch 11/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 6ms/step - loss: 0.4947 - val_loss: 0.4944

Epoch 12/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 6ms/step - loss: 0.4950 - val_loss: 0.4943

Epoch 13/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 6ms/step - loss: 0.4960 - val_loss: 0.4944

Epoch 14/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 6ms/step - loss: 0.4931 - val_loss: 0.4944

Epoch 15/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 6ms/step - loss: 0.4938 - val_loss: 0.4943

Epoch 16/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 4ms/step - loss: 0.4952 - val_loss: 0.4943

Epoch 17/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 5ms/step - loss: 0.4964 - val_loss: 0.4944

Epoch 18/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 5ms/step - loss: 0.4949 - val_loss: 0.4943

Epoch 19/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 6ms/step - loss: 0.4961 - val_loss: 0.4943

Epoch 20/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 6ms/step - loss: 0.4952 - val_loss: 0.4944

Epoch 21/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 4ms/step - loss: 0.4939 - val_loss: 0.4943

Epoch 22/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 4ms/step - loss: 0.4946 - val_loss: 0.4943

Epoch 23/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 6ms/step - loss: 0.4957 - val_loss: 0.4943

Epoch 24/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 6ms/step - loss: 0.4950 - val_loss: 0.4943

Epoch 25/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 6ms/step - loss: 0.4956 - val_loss: 0.4943

Epoch 26/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 6ms/step - loss: 0.4947 - val_loss: 0.4943

Epoch 27/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 5ms/step - loss: 0.4937 - val_loss: 0.4943

Epoch 28/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 5ms/step - loss: 0.4966 - val_loss: 0.4943

Epoch 29/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 6ms/step - loss: 0.4954 - val_loss: 0.4943

Epoch 30/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 5ms/step - loss: 0.4951 - val_loss: 0.4943

Epoch 31/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 5ms/step - loss: 0.4955 - val_loss: 0.4943

Epoch 32/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 5ms/step - loss: 0.4946 - val_loss: 0.4943

Epoch 33/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 6ms/step - loss: 0.4950 - val_loss: 0.4943

Epoch 34/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 6ms/step - loss: 0.4961 - val_loss: 0.4943

Epoch 35/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 5ms/step - loss: 0.4952 - val_loss: 0.4943

Epoch 36/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 4ms/step - loss: 0.4961 - val_loss: 0.4943

Epoch 37/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 6ms/step - loss: 0.4957 - val_loss: 0.4943

Epoch 38/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 6ms/step - loss: 0.4954 - val_loss: 0.4943

Epoch 39/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 6ms/step - loss: 0.4967 - val_loss: 0.4943

Epoch 40/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 6ms/step - loss: 0.4948 - val_loss: 0.4943

Epoch 41/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 6ms/step - loss: 0.4942 - val_loss: 0.4943

Epoch 42/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 6ms/step - loss: 0.4956 - val_loss: 0.4943

Epoch 43/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 6ms/step - loss: 0.4939 - val_loss: 0.4944

Epoch 44/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 6ms/step - loss: 0.4953 - val_loss: 0.4943

Epoch 45/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 5ms/step - loss: 0.4942 - val_loss: 0.4943

Epoch 46/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 6ms/step - loss: 0.4963 - val_loss: 0.4943

Epoch 47/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 5ms/step - loss: 0.4962 - val_loss: 0.4943

Epoch 48/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 5ms/step - loss: 0.4957 - val_loss: 0.4943

Epoch 49/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 5ms/step - loss: 0.4966 - val_loss: 0.4944

Epoch 50/50

[1238/1238 ━━━━━━━━━━━━━━━━━━━━ 6ms/step - loss: 0.4955 - val_loss: 0.4943

saving my model

from tensorflow.keras.models import load_model

model.save('full_data_project_model.h5')

Part 3: Evaluating Model Performance

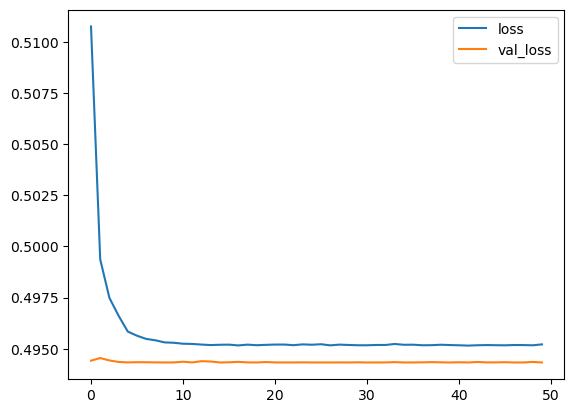

I plotted out the validation loss versus the training loss

loss = pd.DataFrame(model.history.history)

loss.plot()

<Axes: >

I created my our prediction from the X_test set and displayed a classification report and confusion matrix for the X_test set.

y_predict = model.predict(X_test)

y_predict

2476/2476 ━━━━━━━━━━━━━━━━━━━━ 6s 2ms/step

y_predict = pd.DataFrame(model.predict(X_test), columns=['Predicted Y'])

def p_class(x):

if x>0.5:

return 1

else:

return 0

y_predict_class = y_predict['Predicted Y'].apply(p_class)

y_predict_class

0 1

1 1

2 1

3 1

4 1

..

79201 1

79202 1

79203 1

79204 1

79205 1

Name: Predicted Y, Length: 79206, dtype: int64

from sklearn.metrics import classification_report,confusion_matrix

print(classification_report(y_test, y_predict_class))

precision recall f1-score support

0 0.00 0.00 0.00 15493

1 0.80 1.00 0.89 63713

accuracy 0.80 79206

macro avg 0.40 0.50 0.45 79206

weighted avg 0.65 0.80 0.72 79206

confusion_matrix(y_test, y_predict_class)

array([[ 0, 15493],

[ 0, 63713]], dtype=int64)

Part 4: New Case

Given the customer below, would you offer this person a loan?

import random

random.seed(101)

random_ind = random.randint(0,len(df))

new_customer = df.drop('loan_repaid',axis=1).iloc[random_ind]

new_customer

loan_amnt 2000.00

term 36.00

int_rate 7.90

installment 62.59

annual_inc 20400.00

...

zip_code_30723 0.00

zip_code_48052 0.00

zip_code_70466 0.00

zip_code_86630 1.00

zip_code_93700 0.00

Name: 87921, Length: 80, dtype: float64

I had to make sure that my data was numpy array not a dataframe.

new_customer = new_customer.values.reshape(1,80)

new_customer = scaler.transform(new_customer)

y_predict = model.predict(new_customer)

y_predict

1/1 ━━━━━━━━━━━━━━━━━━━━ 0s 40ms/step

y_predict = pd.DataFrame(model.predict(new_customer), columns=['Predicted Y'])

def p_class(x):

if x>0.5:

return 1

else:

return 0

y_predict_class = y_predict['Predicted Y'].apply(p_class)

y_predict_class

0 1

Name: Predicted Y, dtype: int64

I would probably give the loan to this person according to this model prediction.

Here, I checked if this person actually ended up paying back their loan.

df['loan_repaid'].iloc[random_ind]

0

It seemed that the customer had not actually repaid the loan.